Is Warehouse Demand Shrinking?

On June 22nd the Journal of Commerce (JOC) published an article titled "Long-awaited US inventory drawdown spotted" where they state in the first sentence, "Lower US inventories would be a boon from coastal ports to heartland highways". The notable exception to such a boon, as they cite in the next paragraph of the article, is in warehousing demand. If US inventories are reduced we would expect warehouse demand to be reduced as well. However, economic indicators do not support such a drawdown at this time.

The factors JOC cite as indicators of an inventory drawdown include strong truck and steady intermodal traffic in May 2017, steady consumer spending and manufacturing output, increasing inventory costs, and comparatively low transportation costs. While the May inventory to sales ratios have not been released, we can look at each of the indicators cited by the JOC and whether they support an indication of an inventory drawdown.

According to the American Trucking Association, truck tonnage did indeed increase from April to May by 6.5%. However, this follows three straight declines of 2.6% in each of the previous three months. Despite the increase in truck tonnage in May, it remains to be seen if traffic will continue to increase in the future. The ATA Chief Economist, Bob Costello, said "Despite the robust jump in May, I still expect moderate growth going forward as key sectors of the economy continue to improve slowly". US Intermodal Traffic has increased in the last three months to nearly 270,000 Intermodal Units according to the Association of American Railroads. Despite some volatility in traffic over the past year, most monthly readings fall between 250,000 and 270,000 intermodal units. However, volume is clearly down from 2014 and 2015, perhaps from increased competition from the trucking industry and cost cutting actions by the rail carriers.

RTI Dash (1)

fredgraph (1)

Consumer spending, if measured by the Personal Consumption Expenditures (PCE), has been rising steadily over time for decades. While there was a flattening in the rate of increased consumer spending at the end of 2016, the rate has increased since the beginning of 2017.Manufacturing production, as measured by real output, has climbed since January 2014 and, following the 3rd Quarter of 2016, has increased by around 1.1%. However, manufacturing production's role in reducing inventory levels in unclear. For example, raw material inventories may increase concurrently or by even larger amounts with an increase of manufacturing levels. In fact, indexes such as the Institute of Supply Management's PMI® in May 2017 suggest inventories are growing, not shrinking, in the midst of higher manufacturing.

fredgraph (2)

An inventory carrying cost increase would provide an incentive for supply chain participants to reduce inventories across their network. However, according to CSCMP's 2017 State of Logistics Report total inventory carrying costs have declined by 3.2% year over year despite a storage cost increase of 1.8%. The financial cost of carrying inventories fell 7.7% year over year. The aforementioned JOC article cites the same. Again, this data would not suggest that an inventory drawback is imminent based upon inventory carrying costs alone.

Transportation costs, as measured by the Producer Price Index for the Transportation Industry, have been relatively stable since 2014. Year over year costs were up 2% in May but down 4.6% since May 2014. As the ratio of inventory carrying costs to transportation cost rises, supply chain manager would likely draw down their inventory levels. Since inventory carrying costs have been falling and transportation levels stable, the aforementioned ratio is shrinking instead.

fredgraph (3)

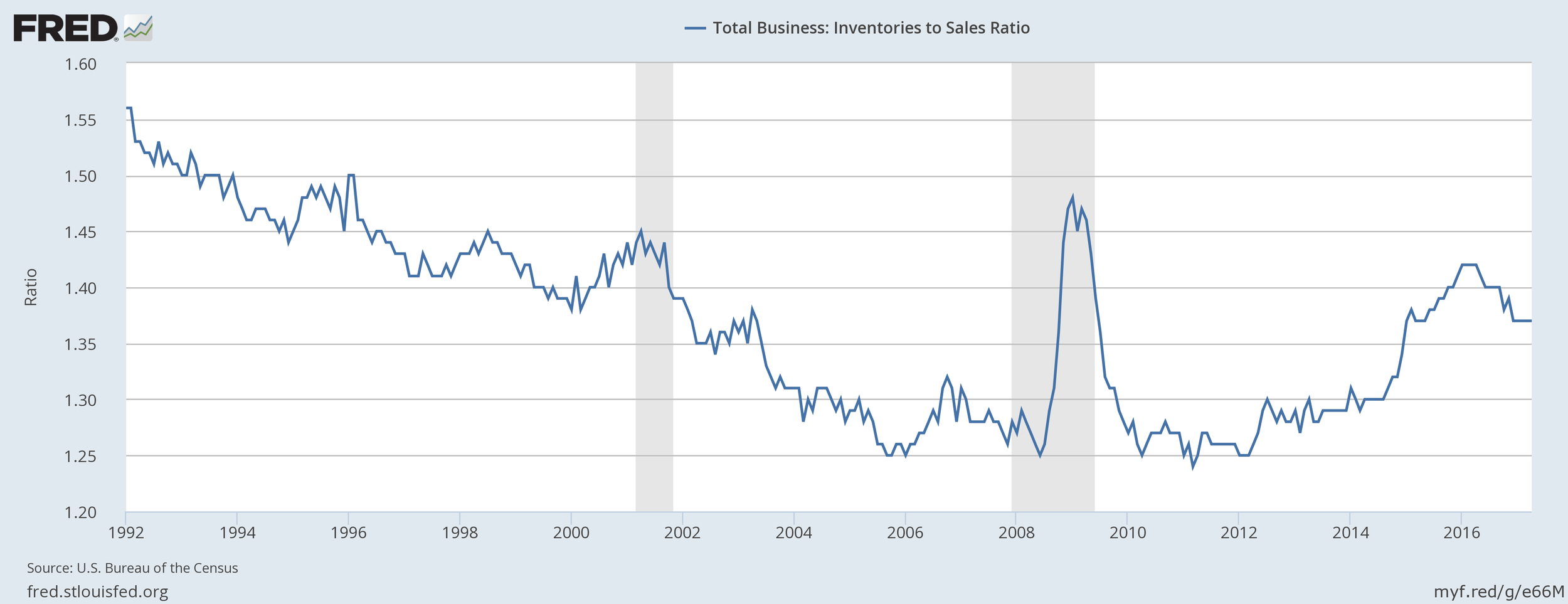

Finally, the inventory to sales ratio has slowly risen since the Great Recession started in 2010. The gradual rise from 2010-2014 rapidly increased in 2015 then has leveled off. There are likely many reasons for the build up in inventory levels since 2015 but the most fundamental is how inexpensive inventory is to hold. Supply chain participants have much less downside by holding inventory than they have risk of stock-outs and other low inventory related issues.

fredgraph

While inventories may very well be reduced in the near future, based on the economic indicators cited here there are no compelling reasons to believe the reduction is happening now.

Just Hit Go! to discuss current market conditions and their potential impact on your company’s real estate today!